Congress Blocked a Retail Fed CBDC Until 2031. Digital-Dollar Control Is Still Alive.

The law is a real brake on one architecture. It is not the funeral for programmable, identity-linked, surveilled dollars that the victory laps suggest.

Congress has blocked the Federal Reserve from issuing a widely available retail central-bank digital currency through the end of 2030.

That sentence is accurate. “Congress banned the digital dollar” is not.

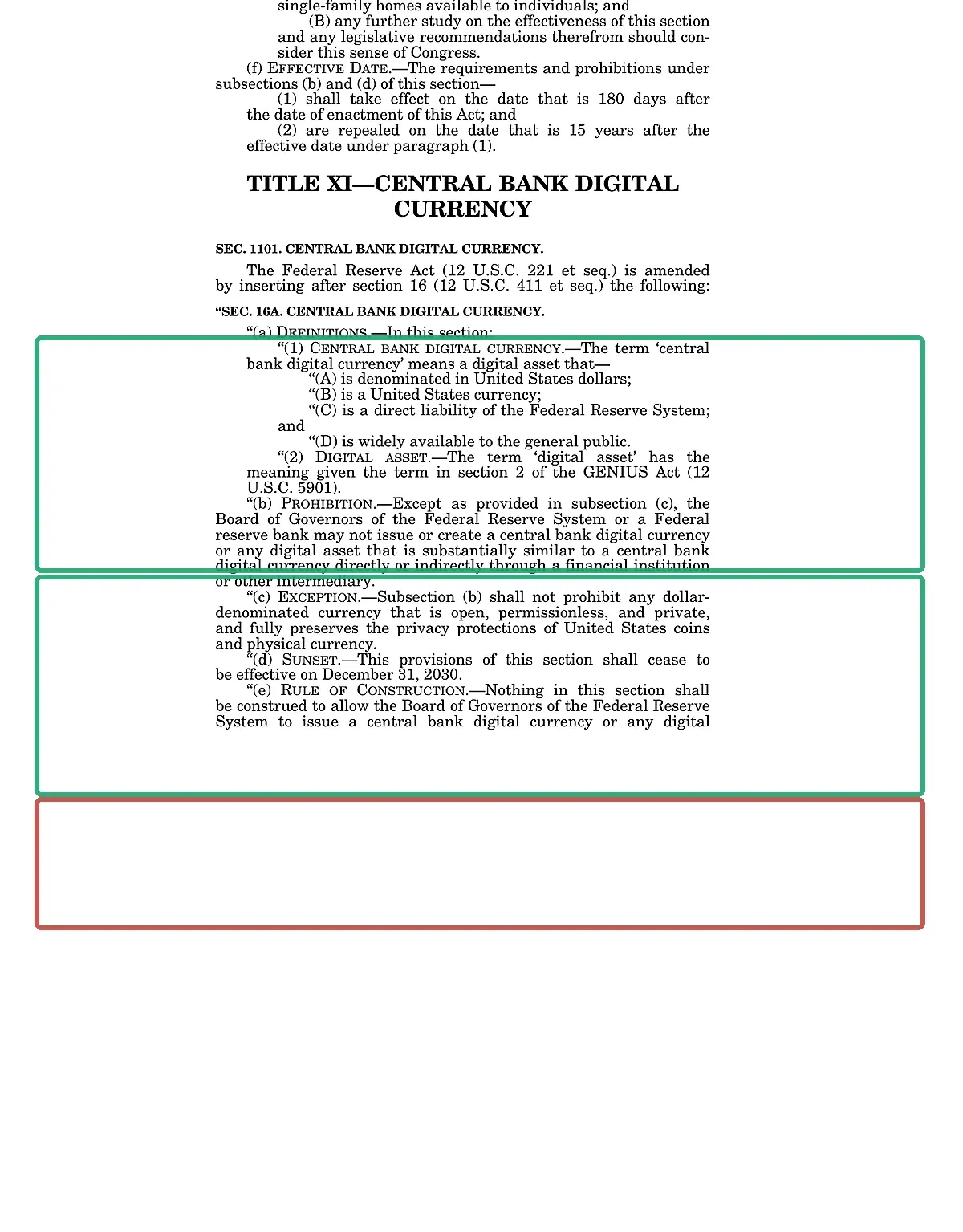

Title XI of H.R. 6644 targets a specific structure: a dollar-denominated U.S. currency that is a direct liability of the Federal Reserve System and is widely available to the general public. It also reaches a digital asset “substantially similar” to that structure and bars the Fed from routing around the rule through a bank or other intermediary.

That matters. A direct public Fed liability would place the central bank at the center of ordinary digital money in a way commercial bank deposits do not. Congress put a temporary wall in front of it.

The rest of the control stack did not evaporate.

Private stablecoins can still carry freeze controls. Banks still conduct identity checks and transaction monitoring. Payment processors can still blacklist accounts. Wallet providers can still become identity gates. A government does not need to give every citizen a Federal Reserve wallet to build a financial system where permission is increasingly software-defined.

The trick is in the liability.

What the law actually says

The House Financial Services Committee and its Democratic minority both announced on July 11 that the broader 21st Century ROAD to Housing Act had become law. The Federal Reserve provision is tucked into Title XI of a housing and community-banking package, because apparently major monetary architecture now travels as carry-on luggage.

The enrolled text defines a covered CBDC using four elements:

- it is denominated in U.S. dollars;

- it is U.S. currency;

- it is a direct liability of the Federal Reserve System; and

- it is widely available to the general public.

The prohibition then says the Fed or a Reserve Bank may not issue or create that CBDC—or a “substantially similar” digital asset—directly or indirectly through a financial institution or other intermediary, subject to an exception.

Page 138 of the enrolled H.R. 6644. Kyber added outline annotations around the definition, prohibition, exception and sunset; the legislative text itself is unchanged. Source: U.S. Government Publishing Office / Congress.gov, public-domain federal record.

The exception is unusually ambitious. It says the prohibition does not cover dollar currency that is “open, permissionless, and private” and “fully preserves” the privacy protections of coins and physical cash.

The text does not build such a system. It does not define how a digital currency proves that it fully preserves cash privacy. It does not settle what “substantially similar” means at the edges. Those are legal and architectural questions, not slogans.

Most important, the section stops operating after December 31, 2030. This is a temporary statutory prohibition, not a permanent constitutional barrier.

The cross-reference makes the scope even narrower

Title XI borrows its definition of “digital asset” from section 2 of the GENIUS Act, now codified at 12 U.S.C. §5901. That provision defines a digital asset as a digital representation of value recorded on a cryptographically secured distributed ledger.

That does not erase the separate phrase “substantially similar.” It does mean the law’s own vocabulary is more specific than “any dollar represented inside a computer.”

Ordinary bank balances are already digital. So are card payments and balances inside payment apps. The Federal Reserve’s 2022 CBDC discussion paper drew the same dividing line: commercial bank account money is a liability of a private entity; a CBDC would be a liability of the central bank.

That difference determines what Title XI directly targets.

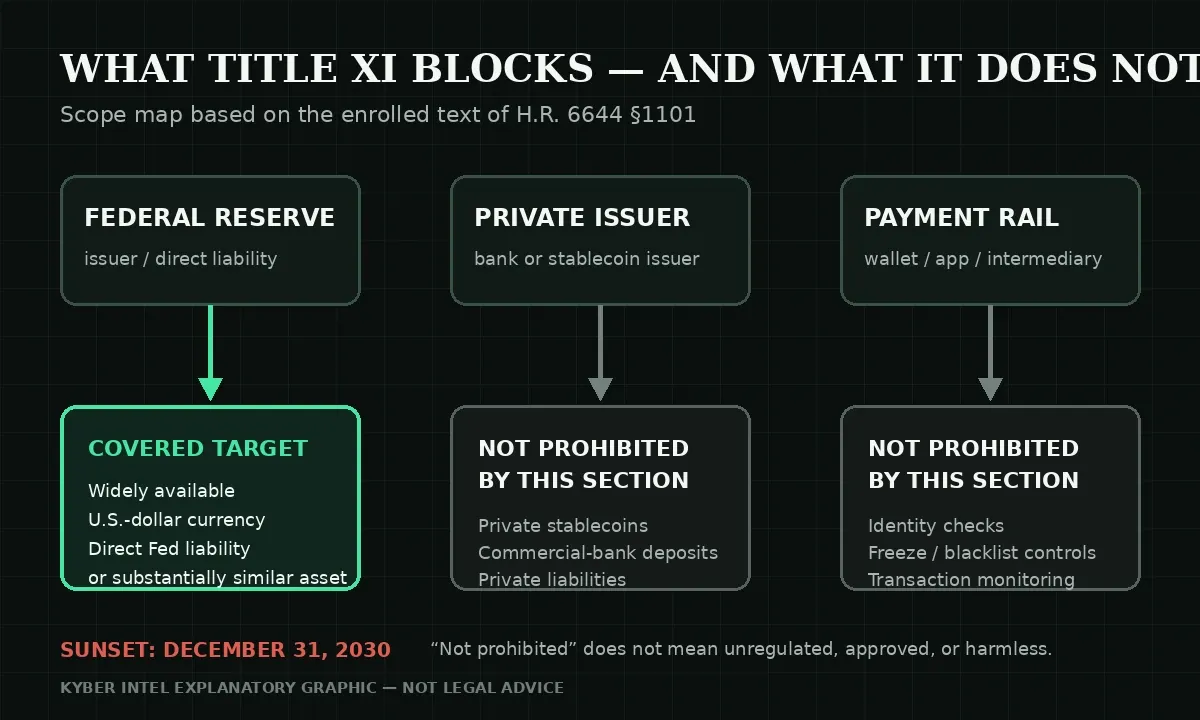

What is blocked—and what is not

Kyber Intel scope map based on H.R. 6644 §1101. “Not prohibited by this section” does not mean unregulated, lawful in every form, approved, private or harmless.

Blocked through 2030

A public-facing, dollar-denominated digital currency that is a direct Federal Reserve liability, plus a substantially similar digital asset, whether offered directly or through an intermediary.

The statute also says nothing in the section should be read to authorize covered issuance without a separate act of Congress.

Not banned by this section

- private stablecoins;

- ordinary commercial-bank deposits;

- existing digital card and bank transfers;

- payment-app balances that are not direct Fed liabilities;

- identity checks imposed by banks, exchanges, wallets or payment processors;

- transaction monitoring, sanctions screening, fraud controls or account blacklists;

- foreign CBDCs.

This is a scope statement, not a blessing. Other laws regulate those systems. Some controls target fraud and serious crime. Some are blunt, opaque or abused. The point is that they remain separate from the retail-Fed-liability architecture Congress just paused.

The wholesale question also needs discipline. Title XI defines a CBDC as widely available to the public. That language does not support claiming every central-bank settlement experiment is banned. The “substantially similar” clause creates uncertainty, but uncertainty is not permission to write the broadest headline possible.

What the Federal Reserve said

The Fed’s most useful public architecture document remains its January 2022 discussion paper. It did not endorse a CBDC. It presented benefits, risks and questions.

The paper said a hypothetical U.S. CBDC would best serve the country if it were privacy-protected, intermediated, widely transferable and identity-verified. It also said the system would need to balance consumer privacy against transparency used to deter criminal activity.

That is the institutional answer: a retail CBDC could offer safe central-bank money and potentially improve payments, while an intermediated design could use private-sector identity and compliance infrastructure.

It is also the conflict in one sentence. “Privacy-protected” and “identity-verified” can coexist in a limited technical sense. They are not the same thing as cash-like anonymity. Privacy becomes a policy setting inside an identity system, which means it can be narrowed by rule, implementation or emergency.

The paper is dated context, not evidence of a 2026 launch plan. The new law is evidence that Congress decided this architecture should not proceed for now.

Why the victory lap is premature

A CBDC is one route to programmable control. It is not the only route.

A regulated private stablecoin can include issuer-controlled freeze or redemption powers. A bank can close an account. A payment processor can deplatform a lawful business. A wallet can require identity verification. A financial institution can produce transaction records under legal process. None of that requires a retail Fed token.

This does not make every compliance control sinister. Targeted investigation, court orders, fraud response and sanctions enforcement are real functions. The civil-liberties problem appears when identity linkage, permanent transaction history and discretionary account control become universal defaults with weak process and no practical exit.

The headline “CBDC banned” invites people to stop watching just as the private rails become more important.

Practical exits: reduce dependency, do not pretend law disappeared

Keep some lawful payment redundancy

Where practical and lawful, do not make one bank, card network, payment app or exchange your only way to pay or get paid. Keep more than one legitimate payment route and document recovery paths for business-critical accounts.

Preserve cash access

Cash remains the most broadly available bearer-style payment tool in the United States. Use it lawfully where accepted. Support merchants and policies that preserve cash acceptance. A theoretical privacy exception in a CBDC statute is not a substitute for physical cash that works now.

Understand who owes you the money

A bank deposit, stablecoin balance, payment-app balance and self-custodied asset are different claims with different failure modes. Record the issuer, custodian, redemption path, freeze authority, recovery method and what happens if the service disappears.

Use self-custody carefully

Self-custody can reduce dependence on an exchange or payment company. It does not remove tax obligations, legal process, software risk, key-loss risk or price volatility. Test recovery with small amounts before treating any wallet as infrastructure.

For people with a lawful need for transactional privacy, Monero is built to conceal transaction amounts and addresses from the public ledger in ways transparent chains are not. That is a technical property, not immunity from law. Follow applicable tax and reporting rules, avoid custodians you do not trust and do not confuse a privacy tool with a magic invisibility cloak.

Track the private control layer

Watch wallet KYC rules, stablecoin freeze functions, sanctions and blacklist procedures, transaction-monitoring expansion, cash-access policy and appeal rights. That is where much of the near-term control fight remains.

Bottom line

Blocking a retail Federal Reserve CBDC through 2030 is a meaningful limit on centralized monetary power. Take the win accurately.

Congress did not permanently ban digital dollars. It did not outlaw private stablecoins. It did not stop banks, wallets or payment processors from linking money to identity and policy. It blocked one defined architecture for a little more than four years.

A free payment system is not secured by changing the logo on the intermediary. It requires cash, competition, self-custody, privacy-preserving options, due process and real ways to leave.

The Fed wallet is paused. The permission layer is still under construction.

Internal reading

- Remote Attestation Is How Your Phone Becomes a Permission Slip

- Phone Unlocking Is the Exit Door Carriers Want to Brick Shut

- The Cloud Is Just Someone Else’s Shortage

Sources

- https://www.govinfo.gov/content/pkg/BILLS-119hr6644enr/html/BILLS-119hr6644enr.htm

- https://www.congress.gov/119/bills/hr6644/BILLS-119hr6644enr.pdf

- https://financialservices.house.gov/news/documentsingle.aspx?DocumentID=411189

- https://democrats-financialservices.house.gov/news/documentsingle.aspx?DocumentID=415375

- https://uscode.house.gov/view.xhtml?req=granuleid:USC-prelim-title12-section5901&num=0&edition=prelim

- https://www.federalreserve.gov/publications/money-and-payments-discussion-paper.htm

- https://www.federalreserve.gov/publications/files/money-and-payments-20220120.pdf